Big Tech's Infinite Advantage, Pt. II: Money as a Weapon

Last post I talked about how the huge advantage of cheap capital lets Big Tech grow and grow into unstoppable giants.

But with even brand-new tech companies getting $100B market caps, the FAANGs and next tier of big tech companies are becoming targets for disruption themselves.

How do they defend their position? Big Tech once again uses the advantage of cheap capital again as a blunt instrument to bludgeon their competition.

They defend their position two ways: acquisitions (the shield) and compensation (the spear). And once again, the market aids and rewards these strategies with sky-stock prices.

The Shield

Facebook’s acquisitions are infamous. The acquisition of Whatsapp for an unprecedented $18B remains shocking given the company had fifty employees and almost no revenue. Facebook was obviously willing to pay any price to buy off its competition.

Zuckerberg could bid confidently, because the deal was 75% stock, meaning FB only paid $4.5B in actual cash. The remaining $14B was not even 5% of the company’s total market cap, a paltry sum to quash an existential threat, and investors were happy to pay.

But FB may not even be the poster boy for this strategy.

As I wrote about before, the “free money” world Big Tech inhabits only exists because they have unlocked a perpetual growth machine. And no one understands this better than Marc Benioff, CEO of Salesforce.

The growth of Salesforce’s core CRM platform has slowed down to the low teens in recent years, but Benioff has made massive acquisitions of younger, faster growing startups an annual affair.

Benioff has grown more bold in using Salesforce’s share price as a weapon to fund acquisitions:

Elon Musk won’t be outdone, of course. In 2019, Tesla issued $1.2B in new shares, followed by a face-melting $12 billion in new issuance in 2020, and investors still rewarded this dilution with a 1000%+ return.

This has helped fund Tesla’s money-losing ways, including the near bankrupt SolarCity business Musk acquired in 2016 for $2.6 billion using 100% stock. Tesla’s recent acquisitions - one in 2020 and two in 2019 - of private, autonomous driving startups were undisclosed terms, but you can bet they were not all-cash.

Morgan Stanley writes in its forecast for record M&A in 2021: “Amid a turbulent business environment last year, companies pursuing stock-for-stock mergers to gain scale comprised many of the largest corporate M&A transactions.”

One could argue the headlines and regulators are so focused on the likes of Facebook and Google, dozens of $100B+ companies are building empires in plain sight.

The Spear

Cheap money keeps the party going, and Big Tech is generous with their invites.

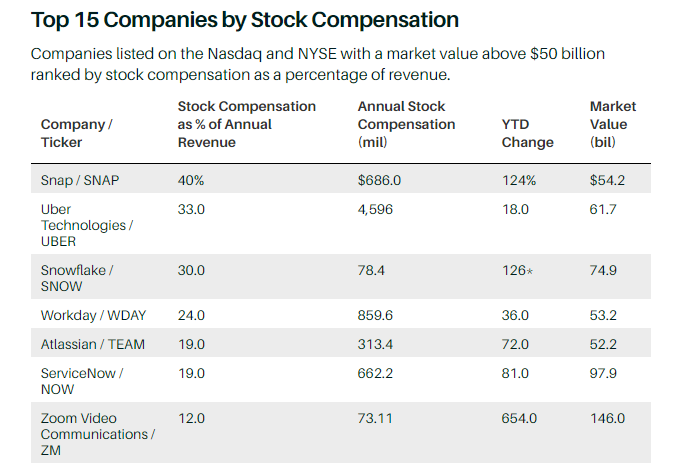

Stock-based compensation (SBC) at large tech companies is an enormous expense. Alphabet alone paid $13B in SBC, nearly $100k per employee.

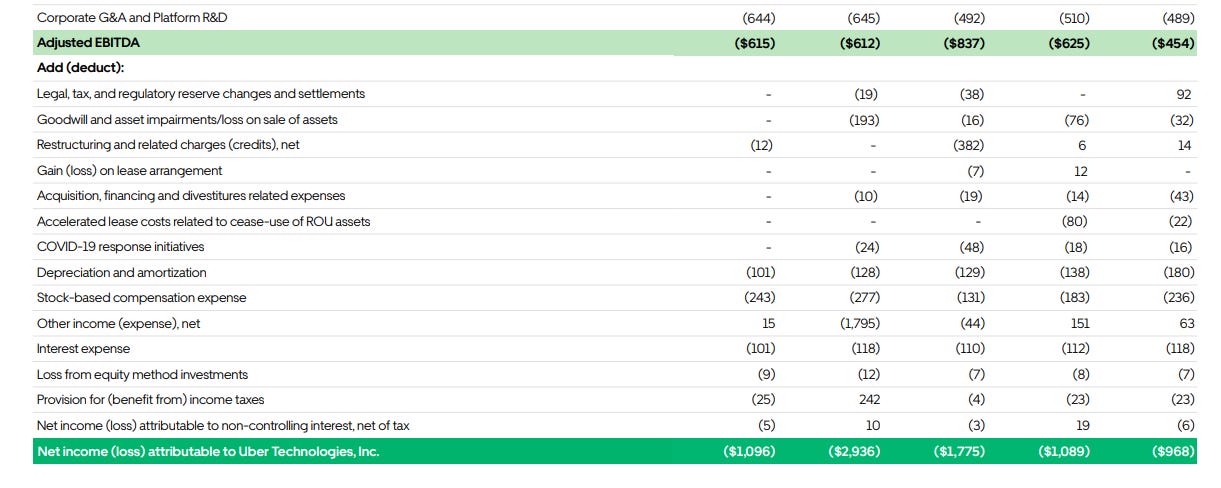

How do tech companies give away so much stock without getting in trouble? Many simply adjust their earnings to remove stock comp from the bottom line - reporting “EBITDA ex-SBC” or simply “adjusted EBITDA” as you might find deep inside Uber’s investor presentation. For Uber, $246M of $514M in adjustments were SBC.

Investors, focused on the underlying metrics of user and revenue growth, look the other way. The list of companies most generous with their stock matches the most popular investments in tech, a straight line from investors to employees’ pockets:

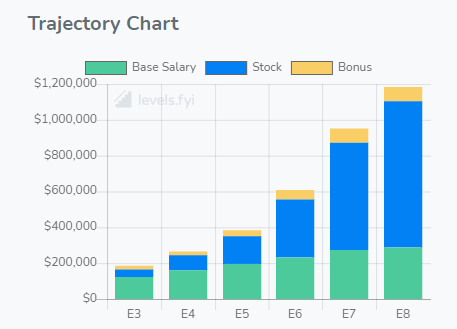

Large tech firms are able to use this sky-high compensation to hire the best engineers and keep them away from competitors.

This chart shows exactly how Facebook generous - with engineering clearing half a million at mid-level roles, and more than half of the comp coming in the form of stock.

Better yet, with all the biggest brains in-house, many of their competitors are likely to never be born. No young startup can come even close to these numbers.

These patterns are even more true for the most cutting edge roles. Quartz estimates large tech firms hired 62.5% of all AI PhDs since 2014: “among e-commerce giants, Amazon holds a crushing lead…[it] hired more than 12 times as many of the top US PhDs as its closest competitor, Chinese e-commerce giant Alibaba.”

All these statistics bring us back to the original question: can new regulations or breakups stop tech’s dominance? And the answer seems to be pretty clear: a resounding no.

Big Tech is taking advantage of what the market gives them. And it’s hard to blame them when investors keep repeating the same mantra:

“We will give you money at any price, no matter how you spend it, as long as you keep growing.”