Big Tech's Infinite Advantage, Vol. 1: The Cost of Capital

Big Tech is coming to kill us all.

Governments are moving to stop them.

I don’t want to write about whether Big Tech is “too big.” It most certainly is. But can efforts to regulate or break them up (partly led by impressive efforts of Friend of the Blog, Lina Khan) limit their power?

The Internet creates network effects that lead to natural monopolies. But the focus on “network effects” obscures another advantage Big Tech has that other industries do not: free money. Amidst all the documentaries on our data, people miss that financial markets are paying these companies to dominate.

How did investors shift away from looking for high profits to paying for moonshots? It all starts with everyone’s favorite billionaire, Jeff Bezos.

The Shift in Narrative

Most businesses try to be profitable, and for basically all of history businesses were valued on their profits. Growth matters more for startups, but profit was the expectation for mature (e.g., billion dollar) businesses.

But Jeff Bezos took an axe to that approach. In 1997, he wrote:

“We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.”

For years, Amazon lived that philosophy. They cared little for profits and used every penny to reinvest in growth. For many years, Wall Street remained cynical. Even in 2015, my professor at Columbia - the famed Bruce Greenwald, “the guru to the gurus” - mocked the Fire phone as a waste of money and declared he was directly shorting it.

The stock has gone up 700% since then.

Google is not much different. The company’s famed “moonshots” division has lost billions for years no, with no signs of stopping.

Why is this such a huge advantage? First, the obvious: if you reinvest 10% every year instead of giving it to shareholders or putting it in the bank, you can outgrow your competitors who don’t. That’s why an e-commerce company that still loses money can outgrow a department store is highly profitable. Over time, a ten percent shift in reinvestment compounds into being multiple times bigger than your nearest competitor.

Cheap Money = Infinite Growth

The other advantage is more subtle. Investors keep piling into these companies even at high valuations. In theory, their cost to get investor money should be high (high beta) but in practice, it is very low: they can raise billions in funding at a higher valuation than anyone else.

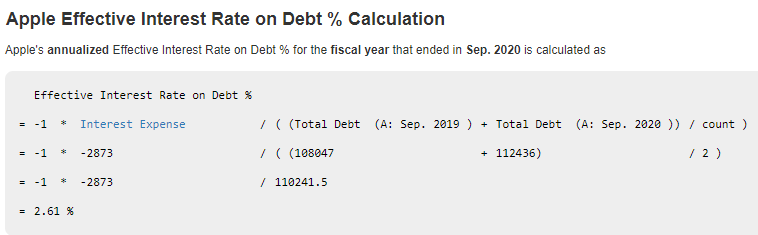

Apple, which often trades at a lower P/E, instead uses debt, which they get for very cheap as well, about 2.6% on average:

That leads to a simple fact of finance: a company can grow as long as the return on investment is greater than the cost of capital.

Cheap money is how Amazon and Google were able to place bets on mobile phone and home device businesses that lost money but would come to dominate mobile search and video subscriptions.

It helped Netflix go from producing a couple originals to hundreds.

And it’s also what will help Apple start car and fitness businesses that will probably lose money but keep users locked into their products forever.

These companies can essentially go after any project, any industry, and take on endless risks - because the market pays them to. And even if they don’t generate profits, it’s the revenues that matter anyway!

Moreover, their cost of capital is lower than their competitors. Mom and pop bookstores are not going to get loans at 2%, if they can get a loan at all. Why should a bank take a risk on lending to a thousand little phone stores when they can write one loan to Apple?

Tech companies know this. In fact, they use the cost of capital as a massive blunt instrument to bludgeon competition and build an even bigger moat. How? I’ll explain more in part 2 next week, but it’s worth noting these advantages are not just applicable to Facebook, Apple, and Google.

In other words, network effects are real. But investors’ belief in network effects also creates a positive feedback loop that infinitely rewards bigness. As my Applied Value Investing professor once said, “When your cost of capital is zero, your valuation is infinity.”

Until the market has reason to change its approach - and regulation might just do that - Big Tech will keep attacking every industry. Break them up, but if investors believe software will keep eating the world, it will.