My book is now on Amazon! + Lessons from the techwreck, part 2

sipping Cathie's inflation kool aid

Exciting news, friends - my memoir on working through the first crypto bubble and collapse, The Billionaire’s Folly, is now available on Amazon!

I wrote it as the Liar’s Poker for crypto - leave me a review and tell me how I did.

It’s been three long years of effort to get this in print, so all I can say is - don’t ever try to write a book! Thanks to Waterside Productions for all their help. If you’re interested in excerpts, check out my previous posts - and I may share more in the future.

And now for the part 2 I promised…

Lessons from the Techwreck, Part 2: Sipping Cathie Wood’s Inflation Kool-Aid

It’s been only three or so weeks since I said it was time to bottom fish tech, and I’m ready to wave the victory flag.

But more seriously, word on the street is that the VC market has frozen up, even after valuations have come down. The surface reasoning is fear over a recession and uncertainty where valuations might eventually land.

But I think there are deeper forces at work. The first inflation scare in decades has upended some long standing assumptions in tech: that you simply chase market share in a large TAM and eventually become “scalable.” The reality is you need pricing power.

Why is this important? Because all our lives prices for everything have gone in one direction: down. But now, software is gasoline on the fire: $1000 a night Airbnbs, $50 to drive one block, $750k salaries on LinkedIn. Data moves faster than atoms, so changing price will always be faster than adjusting production.

The other reason markets are locked up is lack of direction. Investors thought investing in private companies and alternative assets “diversified” their portfolio - but the techwreck showed them all to be identical.

And what does all this mean for those of us sick of paying double for flights and hotels? Is this the new normal?

Leaving the land of plenty

I’m on the record myself as saying tech would drive consistent deflation - cheaper TVs, cheaper phones, and so on forever. If every year more tasks get automated, and we have better data, isn’t it obvious tech was the key to consumer nirvana?

And it did…until it didn’t. It turned out so much of tech deflation - cheaper stuff on Amazon, cheaper mobility - was just a reflection of soft labor markets. But when the job market got tight, it suddenly cost $50 to go one block in Manhattan.

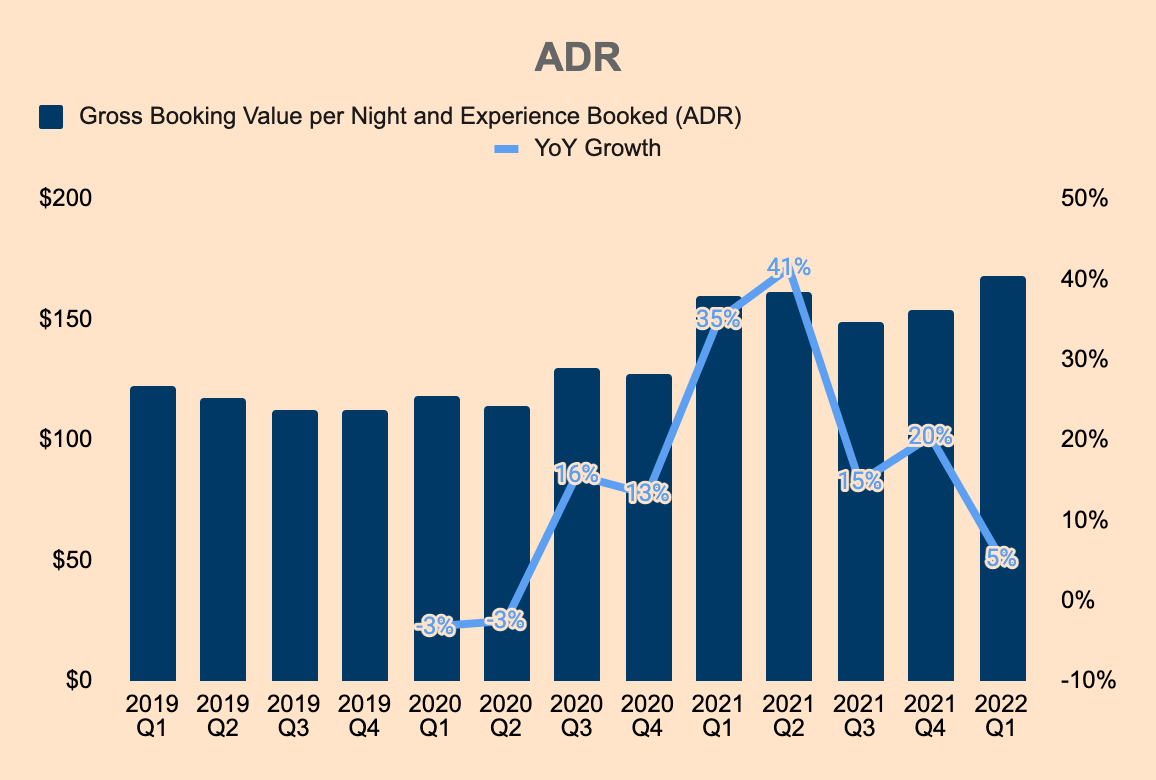

Airbnb theoretically increases the supply of places to stay - and hotel prices were dropping the years before the pandemic. But it also provides hosts with algorithmic pricing. The price per night in an Airbnb was just slightly less than the average hotel room in 2019, but since 2020 has surged much more - nearly 60%, even as hotels are still cheaper.

Airbnb ADR (Average Daily Rate)

US hotel ADRs

How does that change our view of inflation? It shows us what software really does - force markets to clear faster, and there’s usually only one way to do that: changing prices. Shortage of e-scooters? Real-time traffic to the website lets us forecast orders, so we know to increase prices until it stops.

This is equally true for salaries. Sites like Fiverr and Upwork were nice for hiring part-time designers, but when demand for NFTs surged, so did prices for design work. Corporations had power in the past because of opacity - you didn’t know what your coworker got paid. But with levels.fyi, you can get data down to level, location, and role. Salaries on sites like Glassdoor were usually skewed by older data - until the Great Resignation, when a surge in job changes fueled more recent data and let workers know how much they could negotiate.

Not only should this change our view of tech, it should also change how we think about inflation. After fifty years of price stability, inflation episodes like the last two years are more likely as software becomes the market maker of choice, no longer the stock boy or the store manager. But that’s not necessarily scary - because when things go the other way to excess, as they likely will in 2023 - we should anticipate deflation to occur faster as well. And that could spell interesting things for newly digitized markets - like Zillow zestimates and Caravana prices.

The un-Amazon effect and disaggregation theory

“Your margin is my opportunity,” Jeff Bezos said. For years, retailers feared the giant. Customers would walk into a store, try products out, and then see a cheaper price on Amazon and order there instead. This effectively set one competitive price for the entire Internet.

This touches on what Ben Thomson calls aggregation theory. One platform on the Internet can aggregate all of the consumers and wins the market. In Thompson’s view Amazon is not an aggregator because it

But that aggregation has been steadily eroded through years of e-commerce strategy. “One price” no longer exists: memberships like Prime, retailer credit cards, loyalty programs, discount tools like Rakuten and Honey, buy-now-pay-later, subscription-based services for everything from coffee to hair loss supplement, and the overwhelming amount of product choice make it much more difficult to comparison shop.

An Amazon search for any category overwhelms you with results. Consumers are no longer anchored to the cheapest or most popular - because you see three rows of ads first. The “race to the bottom” of cheap Internet goodies has been replaced with a race to the top of the results page - driving up marketing costs.

Ecommerce now is all about disaggregation - developing smaller audiences built around specific niches. Amazon is encouraging that by giving sellers more granular keyword trends than ever. Instagram takes that further. With influencers and micro-influencers, brands want to build an authentic relationship to get the customer thinking about anything other than price. When Amazon was the first window to a product, price was at the top. On an Instagram sponsored post, you don’t even see the price until you’ve clicked through.

All of this flies in the face of the tech-driven deflation thesis. Ironically, by overwhelming them with choice, the Internet exhausts consumers into submission to pay for the product they know will work. And it might be a good thing - making price secondary means Amazon-level scale isn’t the only ingredient to winning.

Beta is still beta

One other obstacle stands in the way of a tech recovery: no one knows how much money to invest.

For years, pension funds and other big funds flooded private markets, seeking alternatives to overvalued stocks. Studies show that innovation provides specific alpha. Theoretically, new asset classes like crypto and pre-IPO companies would enhance the portfolio by providing uncorrelated returns.

And then all of them turned out to be correlated.

Funds like Tiger Global gladly obliged the appetite for private investments - with a supposed added benefit. By buying everything in sight, they made it seem like they could “index” the market.

But the reality is, the private market is dominated by software companies. And most of them are sensitive to more or less the same two factors - enterprise IT spend or millennials’ discretionary income.

And this “crossover” strategy is usually paired with public markets investing - which is now also dominated by tech as well. Meanwhile, the PE landscape is increasingly tech-focused, and crypto turned out to be a proxy for the NASDAQ-100.

You tried to be a good manager and stay close to the index on your public equities, so you were 30% tech. You didn’t want to miss out on exciting startups in private markets, which took you up to 40% in tech. And then the best hedge funds and PE shops were focused on TMT. Then you were 50% tech...what was an asset allocator to do?

Bitcoin’s correlation to the NASDAQ

The obvious answer: sell. And wait.

With illiquid investments that may take years to re-price correctly, it’s impossible to know what your exposure even is. Until that’s more clear, everyone will be stuck doing back of the envelope math and hoping not to get caught offsides.

Really, blame the index makers - at this point, tech should be broken out into multiple sectors. Are we really going to watch its share of the S&P500 rise to 50% or more? Meanwhile, most of the recent IPOs and SPACs languish outside any index, left out in the cold while the party of constant retirement saving keeps flowing into Apple, Google, Microsoft and 497 other companies.

The Rubik’s cube of opportunity cost

Of course, the simplest explanation for the techwreck was that it was a “bubble” driven by easy money. Isn’t that how it always is? Profits didn’t matter because of the Fed, etc.

But that likely oversimplifies things. The unicorn era also blossomed thanks to an unprecedented run of price stability, deflation in computing costs (e.g., the 66 price cuts to AWS), and the biggest generation in American history hitting peak spending power.

There’s really two analogies to look at the tech “economy” now. One is farmland that’s been abused with chemical fertilizer, where VCs have exploited every opportunity that they could, leaving nothing but dust for the future.

The other is a pet that outgrew its litter, ate too many snacks and then made a mess. But that doesn’t mean you stop feeding the kitten, because he’ll still grow. Onerous IPO regulations and investor accreditations kept him sheltered from the real world for too long.

So which economy are we in? One where there’s still plenty of ideas to invest in, or a fake one run on stimulus? The flood of cash into markets in 2020 and 2021 tells me that investors were simply too conservative in the years running up to the pandemic boom, and not conservative enough once things got going.

Perhaps they were worried about their soon-to-retire boomer stakeholders - or, excess inequality in the US left too much idle cash in the hands of the rich. (Likely both!) Is it low rates that leads to the idle cash, or is it too much idle cash and inequality that causes low/yield rates? That’s the puzzle that only time and policy will reveal. As we enter an unprecedented era of depopulation, rising rates, and growing automation, I can promise history will be no guide.